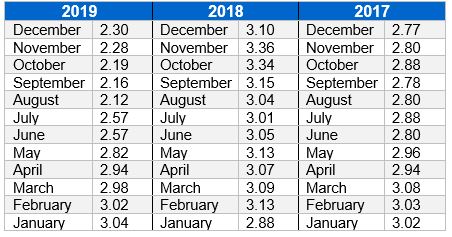

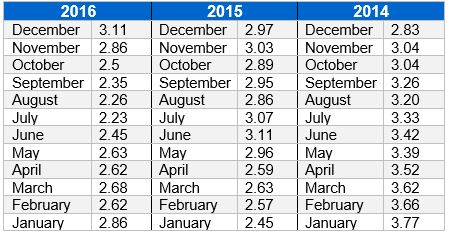

GATT Rates

GATT rates are often used with companies that have large pension programs to calculate lump sum distributions, including local companies. The GATT rate is equal to the 30-year Treasury bond interest rate. Please contact us with any questions on how the changes in these rates affect your pension.

Source of Rates: IRS Official GATT Rate Information Tables

*Note regarding ERISA 4022 immediate and deferred lump sum interest rates - On September 9, 2020, PBGC issued a final rule providing that, starting in 2021 PBGC will use rates published by IRS [i.e., the IRC 417(e)(3) rates] to determine lump sum amounts for plans terminating after 2020. Because of that change, the December 2020 immediate and deferred rates shown in the November 2020 Monthly Interest Rate Summary were the last “legacy” 4022 rates that will be published. The final rule contains a table that enables practitioners to determine immediate and deferred interest rates in accordance with PBGC’s historical methodology for months after December 2020. Individuals seeking information about the interest rates their plans use to determine lump sums should contact their plan directly.